12.9.1 Commercial beef farm record keeping

Record keeping is the only method to obtain perspective of any agricultural enterprise. Cattle farmers are known not to do much about records of their farming operations except for the numbers of their cattle. This is not good enough as it says very little about production and several other important aspects to be recorded or controlled. Data capturing within an enterprise is the only way to collect data for processing to obtain intelligence, or to make business sense out of the data.

Remember the saying: ‘’You can’t manage what you can’t measure’’.

One has to see a farming operation in a holistic context embracing much interesting and noteworthy information. For that reason, a number of subjects are listed in a table format. At the end of each year, one has to evaluate the date of each table and one can design the sheet the way one likes. The main thing is to believe in the value of such information and keep it for comparisons with previous years’ data. In this way the farmer is accumulating statistics which are very valuable and nowhere else available.

Participation in study groups with other farmers in your district is another sensible way of sharing data, getting new ways of collecting and analysing data, in order to compare yourself with the reproduction averages in your district.

Identification of cattle is a must. Calves should be identified with earmarks soon after birth. At weaning they should be branded with a letter-code of the year and season of birth on the left hip. All breeding stock should have an ear tag to show their number and year of birth.

12.9.2 Contents of records

- The Start-up Inventory

- Monthly numbers and activities

- Calving season records

- Camp utilisation records

- Cattle slaughter data

- Sales of weaners

- Cattle herd production records

The cattle herd’s production records are by far the most important. This information represents the essence of a cattle herd’s performance and reflects the ability of management to utilise a sustainable interaction between ecology and beast. Together with information on the slaughter-performances, it will also reflect the soundness of the cattle type’s ability within the system. So, it is fully justified to state that we are now dealing with all the answers to the question of ‘’what is cattle farming’’.

|

· Cattle herd’s performance · Interaction between ecology and beast · Slaughter-performances · Soundness of the cattle type |

To present a cattle herd’s performance this way asks for a lot of preparation before it can be tabled as is shown. The annual preferential date to weigh the whole cattle herd is at the end of February.

After all the physical exercises are done, it is truly the most pleasant administrative action to do the necessary calculations and complete the table as it is presented. Answers to the seven efficiency criteria items in the table (to be completed) secures a farming operation on to the highest level in agricultural science and opens opportunities for comparisons with any cattle farming enterprise in the country and also beyond our borders. Hopefully one day this could be done on a large scale involving different breeds and various regions of the country which will lead to opportunities for valuable statistical analyses and research in cattle farming.

Opening and closing stock

“Opening stock is the value of goods available for sale in the beginning of an accounting period. Closing stock is the value of goods unsold at the end of the accounting period.”

Cattle farming has two natural components to manage: veld and cattle. Controlling the utilisation of the veld is straightforward, as is the number of cattle. To integrate those two components successfully is one of the most important managerial requirements of running a cattle farming enterprise.

The nutritional requirements of livestock / cattle are calculated in terms of their live mass. Because of the differences in cattle classes, as well as between breeds, it is necessary to work with a herd’s live mass in combination with its numbers. The comparison of one Nguni cow with a Simmentaler cow, being animal units, is not justified, nor is the comparison of 200kg weaner with a cow of 500kg. A herd of 400 Nguni cows weighing 144 000kg (@ 360kg per cow) should only be compared to its equivalent live mass in Simmentalers, which is 288 cows at 500kg per cow.

So when it comes to record keeping of livestock production, one has to measure the live mass of a cattle herd at the beginning and at the end of a production year, as well as the live mass marketed from the farm. This is the only way to obtain significant values of what production is about.

12.9.3 Start keeping records:

12.9.3.1 Step 1: The Inventory

For a new farmer to start off, gather all animals in the handling facility that is equipped with a neck clamp and preferably a cattle scale, or weight belt. Let the animals exit the handling facility through the crush and neck clamp, and start recording the following data according to the technical knowledge you gained during the training, which includes the sex, aging through checking the teeth, and getting the weight though weighing, measuring with a weight belt, or a good estimation, to start with.

This inventory is a once off exercise and you use the format of the tables below to record and categorise your total herd of cattle.

It is important to remember that the exercises that follow are only theoretical models to simulate examples of reality. The correct time to weigh your stock will be at the beginning of the financial year, being 1 March every year. For this exercise, we only make an example to weigh all animals when doing the inventory.

Assumptions

Farmer Dhlamini has 58 cattle on his farm Evian, in extent 500 hectares. He never kept any records, except knowing the totals in his mind. Farmer Dhlamini will thus start with gathering all his cattle in the kraal, chasing them one by one through the crush, immobilize them in the neck clamp, most probably over a scale or he will estimate the weights with the use of a weigh belt, check the tag numbers, or create a new numbering system and apply new ear tags to the ears, check the teeth for aging, and start recording an inventory according to the following example.

Table 1: Record/ Inventory of cattle numbers according to the different categories of the herd.

|

Cattle inventory |

||||

|

Bulls |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Nguni black and white |

4 |

A003 |

289 |

|

2 |

Brahman white |

8 |

BB222 |

525 |

|

3 |

|

|

|

|

|

4 |

|

|

|

|

|

Etc |

|

|

|

|

|

Totals |

2 |

|

814 |

|

|

Dry Cows (Not- pregnant) |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Cow |

3 |

124A |

325 |

|

2 |

Cow |

4 |

125B |

455 |

|

3 |

Cow |

6 |

116S |

380 |

|

4 |

Cow |

8 |

174S |

400 |

|

5 |

Cow |

4 |

200D |

425 |

|

6 |

Cow |

4 |

520F |

384 |

|

7 |

||||

|

8 |

||||

|

Etc. |

||||

|

Totals |

6 |

|

2369 |

|

|

Dry Cows (Pregnant) |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Cow |

6 |

125F |

420 |

|

2 |

Cow |

4 |

888H |

390 |

|

3 |

Cow |

3 |

864D |

380 |

|

4 |

Cow |

6 |

333S |

280 |

|

5 |

Cow |

8 |

121W |

300 |

|

6 |

Cow |

3 |

WSJ32 |

320 |

|

7 |

Cow |

7 |

WhR2 |

340 |

|

8 |

Cow |

7 |

778G |

290 |

|

9 |

Cow |

5 |

775S |

350 |

|

10 |

Cow |

3 |

898F |

405 |

|

11 |

Cow |

4 |

875R |

380 |

|

12 |

Cow |

6 |

333S |

280 |

|

13 |

Cow |

8 |

121W |

300 |

|

Etc. |

|

|

|

|

|

Totals |

|

13 |

|

4435 |

|

Lactating Cows |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Cow |

4 |

012C |

350 |

|

2 |

Cow |

5 |

F435 |

380 |

|

3 |

Cow |

5 |

322S |

480 |

|

4 |

Cow |

7 |

G453 |

350 |

|

5 |

Cow |

8 |

658R |

420 |

|

6 |

Cow |

4 |

500F |

400 |

|

7 |

Cow |

3 |

287R |

380 |

|

8 |

Cow |

4 |

1003A |

390 |

|

9 |

Cow |

6 |

2018F |

285 |

|

10 |

Cow |

6 |

1168S |

305 |

|

11 |

Cow |

4 |

1031S |

300 |

|

12 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

11 |

|

4040 |

|

|

Sucking (Milk) Calves |

||||

|

No |

Description |

Age (Month) |

Mark / No |

Weight (Kg) |

|

1 |

Heifer |

2 |

11/18/01 |

80 |

|

2 |

Heifer |

1 |

12/18/07 |

45 |

|

3 |

Bullock |

2 |

11/18/04 |

65 |

|

4 |

Heifer |

2 |

11/18/09 |

75 |

|

5 |

Bullock |

2 |

11/18/05 |

80 |

|

6 |

Bullock |

1 |

12/18/02 |

40 |

|

7 |

Heifer |

2 |

11/18/11 |

85 |

|

8 |

Heifer |

2 |

11/18/08 |

80 |

|

9 |

Bullock |

1 |

12/18/03 |

48 |

|

10 |

Bullock |

2 |

11/18/10 |

80 |

|

11 |

Heifer |

1 |

12/18/06 |

38 |

|

12 |

|

|

|

|

|

13 |

|

|

|

|

|

14 |

|

|

|

|

|

15 |

|

|

|

|

|

16 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

11 |

|

716 |

|

|

Weaner (Heifers) |

||||

|

No |

Description |

Age (Month) |

Mark / No |

Weight (Kg) |

|

1 |

Heifer |

7 |

06/18/001 |

285 |

|

2 |

Heifer |

7 |

06/18/004 |

275 |

|

3 |

Heifer |

7 |

06/16/003 |

280 |

|

4 |

Heifer |

6 |

07/18/002 |

260 |

|

5 |

Heifer |

8 |

05/18/005 |

290 |

|

6 |

|

|

|

|

|

7 |

|

|

|

|

|

8 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

5 |

|

1390 |

|

|

Weaners (bull calves) |

||||

|

No |

Description |

Age (Month) |

Mark / No |

Weight (Kg) |

|

1 |

Bullock |

7 |

06/18/012 |

250 |

|

2 |

Bullock |

8 |

05/18/011 |

280 |

|

3 |

Bullock |

7 |

06/18/007 |

290 |

|

4 |

Bullock |

7 |

06/18/009 |

280 |

|

5 |

Bullock |

7 |

06/18/010 |

275 |

|

6 |

Bullock |

7 |

06/18/007 |

250 |

|

7 |

Bullock |

8 |

05/18/008 |

270 |

|

8 |

Bullock |

8 |

05/18/006 |

280 |

|

9 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

8 |

|

2175 |

|

|

Steers / Oxen |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Brown and White Ox |

8 |

C323 |

520 |

|

2 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

1 |

|

520 |

|

|

Other |

||||

|

No |

Description |

Age (years) |

Mark / No |

Weight (Kg) |

|

1 |

Piet labourer’s black ox |

6 |

P222 |

850 |

|

2 |

|

|

|

|

|

Etc. |

|

|

|

|

|

Totals |

1 |

|

850 |

|

Note 1: Looking at the numbers of the animals, it can be noted that farmer Dhlamini most probably obtained animals from various suppliers with different number codes that do not make sense at all. In cases like this, it would be a good practice to replace all existing ear tags with a new numbering system that will correlate with the new and future data of the farm.

|

001 2017 |

For example:

On the new replacement ear tag above, farmer Dhlamini indicated that the cow was re-marked as number 001 on January 2017.

Note 2: Dry cows being pregnant or non-pregnant? This matter is not important when making the first inventory as the inventory will serve no further function after the herd numbers are transferred to the Monthly Cattle Chart as explained below. In this exercise we presume that farmer Dhlamini could differentiate between pregnant and non-pregnant dry cows through observation and with the help of his herdsman with years of knowledge of the cows. In the future, the status of pregnancy after the mating season will most probably be determent by a Vet (State Vet) on request of farmer Dhlamini.

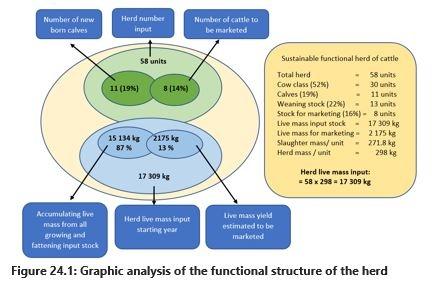

12.9.3.2 The functional structure of the herd inventory

This knowledge was already explained in the previous parts of this course, but it is important for you to understand the functional structure of the inventory compiled in step 1 above.

Figure 1 below is a graphic analysis of the functional structure of the herd compiled from the inventory.

Assumptions for understanding Figure 1:

There are 8 weaner bulls (16%) of the herd to be marketed at a total weight of 2 175 kg (16%)

All growing and input stock is the total input weight of all breeding animals, e.g. bulls, dry cows, lactating cows, suckling calves, replacement heifers and other stock not immediately marketed such as the 2 Oxen. Although farmer Dhlamini’s labourer Piet owns one ox, this ox must be considered and counted as part of the herd on the farm, as it is also consuming resources such as natural grazing.

12.9.3.3Step 2:

Transfer the opening stock cow totals to the monthly cattle card

The Monthly Cattle Numbers Card is very important and must be completed at the end of every month. The opening balance arrives from the previous month’s end-balance. When the numbers of a class decrease due to a change from one class to another, it must be shown as “transfer” under “decrease” and as well as “transfer” under “increase” of the classes involved.

To calculate the percentage composition of the various classes in the herd from the figures in the card at the end of every month is easy and valuable information to fill in.

All management actions undertaken must also be noted on the cards, like immunisations, branding, etc. with the date as well.

After completing all the Monthly records, the next step will be to focus on calculations of production of the herd in terms of its INPUT, OUTPUT and EFFICIENCY criteria shown later on.

12.9.3.4 Calving season records

The priority of the Calving Season Record card is to list the birth of calves in terms of their date of birth, their sex, and the number of the dam. If different bulls are used, or different breeds of bulls, and this can be identified, it is useful to mention on the card.

This card will also serve for recording the weight at weaning as well as the weight of the mother, if available. At this stage it is also due time to put a brand on the left hip of the calf to show the season and year of birth. For instance, if the birth was in the summer of 2017, the code will be S17. If the birth was in the winter of 2018, the code will be W18.

Remember to record these activities on the Monthly Cattle Numbers card.

12.9.3.5 Cattle herd production data

Production of cattle farming is based on the production performance of its cattle herd as a whole versus its live mass. This information represents the essence of the existence of a cattle herd and reflects the ability of management to utilise a sustainable interaction between ecology and beast. Together with the information on the slaughter-performances, it will also reflect the soundness of the cattle type’s ability within the system.

The reason for working with the live mass of a cattle herd is obvious because the nutritional requirement of livestock / cattle is calculated in terms of its live mass. Because of the differences in cattle classes, as well as between breeds, it is necessary to work with a herd’s live mass in combination with its numbers. The comparison of one Nguni cow with a Simmentaler cow, being animal units, is not justified, as is the comparison of 200 kg weaner with a cow of 500 kg. A herd of 80 Nguni cows weighing 28 800 kg (@ 360 kg per cow) should only be compared to its equivalent live mass in Simmentalers, which is 52 cows at 550 kg per cow.

To present the performance of a cattle herd asks for a lot of preparation before this can be tabled. One has to realise that production per se means nothing unless it is in context of an input. Therefore, one needs an input value of a cattle herd, which is an average of the herd through the year. The only way to obtain this (input) is to measure the herd’s live mass at the beginning and end of a production year and divide it by two. To obtain production, one needs to record the live mass of the cattle marketed from the farm during the same year as well as increases of numbers and kilogram live mass for the 12 months beyond the beginning of the year.

In the case of this example, the cattle’s detail on the inventory is taken at the beginning of the production year. 12 Cards are shown thereafter to show the monthly details of management and variation of numbers per class, new births, marketing and transfers from one class to another. See how the final table is structured.

The information on this card is divided into Input Data, Output Data and Efficiency Criteria:

- The Input Data is arrived at from lists of weighing data of the herd on local A4 paper at the commencement and end of each production year. It is recommended that the weighing data should be processed in terms of the various classes of cattle. After processing the detail of each cattle class, the results are written on this card where it belongs (see the card). Input is the average of values at the beginning and end of each year, as is shown on the card. The main input-figure-values are those stipulated in the third column, highlighted in brown on the card. The other figures of the different cattle classes are valuable to study in terms of variation from one year to the other.

- The Output Data is arrived at from the separate local lists of cattle marketed and processed in terms of the total number of cattle and their total live mass.

- Evaluation: Efficiency Criteria: There appear seven criteria to be processed from the information supplied above. Each represents a relation or proportion. In the beginning the figures will appear to be of little value. Those items can only be valued in a holistic context and become more meaningful / significant after being compared with similar data from elsewhere, or over years to follow.

12.9.3.6 Sales of weaners

Weaner calves are normally sold directly via an agent of a feedlot, over a scale on the farm, loaded and taken away.

The agent will supply a written voucher of the numbers and weights, as well as the price offered, negotiated and accepted by the farmer.

When weaners are removed for the farm, they are taken off the herd records, but the statistics regarding age, weight, grade, price per unit and total price received becomes part of the management data for analysis to take better management decisions in the next production season.

A simple card for analysis can be drafted according to the example below.

12.9.3.7 Cattle slaughter data

The final product of a cattle farm is the carcasses of the cattle marketed to abattoirs. The farmer/cattle owner should always be present when a batch of cattle is slaughtered. He is now in the position to judge the quality and weight of the carcass. The agent at the abattoir will supply each producer with a printout report of the carcasses from which he can fill in all the data needed for the Cattle Slaughter Data card. One card is needed for each batch of cattle marketed.

12.9.3.8 Camp utilization records

Purpose

The purpose of camp-records is to control the amount of utilisation of camps. A record card must be available per camp per annum. The camp-card makes provision for an estimation figure of the capacity of grazing available at the beginning of each year in terms of grazing days, which could vary from year to year. The criteria used are not exact values as it depends on estimations. When cattle enter and depart from a camp their detail must be noted on the card.

The utilisation card for camps has a heading where the details of the camp must be filled in. It begins with the name of the cell or post where the camp is situated. Then it refers to the name/number of the camp, followed by the size of the camp and then by the capacity in grazing days for one year.

To work out capacity is as follows: 365 (days) x 120 (hectare) ÷ 8 (hectare/LSU) = 5475 grazing days.

To obtain a value for LSU, one needs to take an average live mass figure for the cattle herd of a farm as base. For medium framed breeds it is normally about 340kg. For a small framed breed like Nguni, it is about 220kg.

When the camp is used for 20 days, stocked with 40 weaners valued at 0.6 LSU’s, the results are:

- 20 days x 40 weaners x 0.6 LSU = 480 days

So, after the above period of grazing, the availability capacity is: 5 475 – 480 = 4995 days.

If the camp is used again at a later stage by 50 cows valued at 1.4 LSU for 15 days, the results are:

- 50 cows x 15 days x 1.4 LSU = 1050 days, and available grazing now is 3945 days (4995-1050).

12.9.4 Financial records

12.9.4.1 Introduction

It is expected from the modern commercial beef farmer to not only have enough technical knowledge on beef production, but also to be able to keep records of production outputs in order to measure those outputs with the aim to always improve production outcomes whilst spending less money on production cost, or to improve production efficiency.

The recording of financial records leads to financial statements, and financial statements are the final evaluation report on how successfully you managed your business. The business financial records of your farm will be the final evaluation card for a bank or financing institution to consider a loan or capital investment in your business.

Financial record keeping is a logical process and involves good financial planning (budget), recording of all incomes versus expenses (income statement), the management of a well-planned cashflow situation (cash flow budgets), and ultimately the final statement, being a balance sheet.

Financial statements show you where the money for a business came from, where it went, and where it is now.

It is sad to say, but many commercial farmers still believe that financial record keeping is the job of a bookkeeper. Therefore, they will “file” all source documents by throwing these in a box and taking it together with the annual set of bank statements to an accountant at the end of the financial year, just to keep “SARS” happy.

“It is sad to say, but many commercial farmers still believe that financial record keeping is the job of a bookkeeper just to keep SARS happy! “

There are a few important principles to follow in order to keep financial records practically, AND to use such records as valuable management criteria.

“Financial records / statements are about: “Show me the money!”

12.9.4.2 Logical flow / sequence of financial records:

Financial record keeping also starts with an inventory, but the difference is that you will add a value to the item listed. In a new business with no financial records, or even an existing farming venture with no formal financial records, you will have to start collecting financial records in the following logical sequence.

12.9.4.3 Step 1. Inventory of Assets and Liabilities = Balance Sheet

Start with an inventory of all the assets on the farm. This will help you to draft your first balance sheet. The first balance sheet will immediately tell you where you stand regarding what you have in assets, but also as to what you owe in debts.

The balance sheet compiled from the very first inventory is the first benchmark document against which you will compare the end of the financial year, after keeping real time financial records.

12.9.4.3.1 Annexure D:

Inventory and opening balance sheet

|

Description |

Quantity |

Value per unit |

Current value |

|

1. Land |

|||

|

Farm Evian |

500 ha |

R 4 500.00 |

R 2 250 000.00 |

|

TOTAL LAND |

|

|

R 2 250 000.00 |

|

2. Livestock |

|||

|

Breeding bull |

2 |

R 47 000.00 |

R 94 000.00 |

|

Breeding Cows |

50 |

R 10 000.00 |

R 500 000.00 |

|

TOTAL LIVESTOCK |

R 594 000.00 |

||

|

3. Machinery and Equipment |

|||

|

MF 165 Tractor |

2 |

R 65 000.00 |

R 130 000.00 |

|

Trailer |

1 |

R 12 000.00 |

R 12 000.00 |

|

Disc |

1 |

R 6 500.00 |

R 6 500.00 |

|

Toyota Hi-Lux LDV 2015 |

1 |

R 150 000.00 |

R 150 000.00 |

|

TOTAL MACHINERY AND EQUIPMENT |

|

|

R 298 500.00 |

|

|

|

|

|

|

4. Production stock on hand |

|||

|

Lucerne seed 25 kg |

10 |

R 12 500.00 |

R 125 000.00 |

|

Phosphate blocks cattle |

15 |

R 465.00 |

R 6 975.00 |

|

TOTAL PRODUCTION STOCK ON HAND |

|

|

R 131 975.00 |

|

5. Products on hand |

|||

|

Maize bags 40 kg |

2500 |

R 84.00 |

R 210 000.00 |

|

|

|

|

|

|

TOTAL PRODUCTS ON HAND |

|

|

R 210 000.00 |

12.9.4.4 Step 2. Enterprise budgets

The different commodities which you are producing on the farm are called enterprises. The enterprise budget is also discussed in earlier modules of this course, and will tell you whether the enterprise is making a profit, or loss, and whether it is worth it to proceed in farming with an enterprise that is making a loss. It is important that enterprises must not subsidise one another year after year. Rather focus on those enterprises that are profitable.

An enterprise budget is a listing of all estimated income and expenses associated with a specific enterprise to provide an estimate of its profitability. A budget can be developed for each existing or potential enterprise in a farm plan and provides benchmarking information that is of crucial importance in the decision-making process between different production enterprises on the farm. Beef cattle producers will for example also produce maize, or lucerne, or other fodders to supplement the natural grazing resource.

12.9.4.4.1 Annexure E:

Enterprise budget

Projected budget for farmer Dhlamini from his initial inventory

Assumptions:

- Farmer Dhlamini is planning to sell his existing 2 bulls and the replace them with 1 top-class Bonsmara bull at R 35 000.00

- The 8 weaner bulls will be sold to the feedlot

- The directly allocatable cost to maintain the 30 cows plus 5 heifers is indicated

12.9.4.5 Step 3. Holistic farm budget

The budget is an estimate of income for a set period of time, normally a financial year, or a production season. The normal financial year of cattle farmers stretches from the 1st of March up to 28 February of the following year.

A holistic farm budget is now compiled from the various enterprise budgets. This budget will indicate the overall income of sales from products, against the cost of sales, plus other planned costs such as rent, salaries, bank costs, etc. No business can function without a proper budget! As you are doing business during the year, the real expenses and income must be compared with the budgeted income and expenses. This will give you a real sense of where you stand financially

12.9.4.5.1 Annexure F : farm budget

12.9.4.6 Step 4. Cash flow budget

The cashflow budget is your projected monthly income statement and will be controlled against real monthly income and expenses recorded in your income statement. Cash flow statements report the inflows and outflows of cash in a business. This is important because a business needs to have enough cash on hand to pay its expenses and to purchase assets. While an income statement can tell you whether a company made a profit, a cash flow statement can tell you whether the company generated cash.

A cash flow statement shows changes over time rather than absolute rand amounts at a point in time. It uses and reorders the information from the balance sheet and income statement.

The bottom line of the cash flow statement shows the net increase or decrease in cash for the period.

Cash is King…as cash flow is the heart of your success. But cash flow needs to be well planned and managed!

12.9.4.6.1 Annexure G

12.9.4.7 Step 5. Record and update the Income Statement.

Always apply the following golden rules:

Your bank account and your monthly bank statements received from the bank are some of the most important and valuable source documents to legally prove and state your financial position. Bank Statements are nothing else than a legal monthly income statement. If you do not use a bank account in this responsible way, how else will you legally prove your income and expenses, and how will you ever expect the bank to invest in your farming business?

12.9.4.7.1 Annexure H

Income Statement

Income Statement for the financial year 1 March 2019 until 28 February 2020

Farmer Dhlamini

|

Income |

Amount (R) |

|

Sales livestock |

105 800.00 |

|

Sales crops |

83 700.00 |

|

Government payments |

3 600.00 |

|

Contract work |

6 600.00 |

|

Total Income |

199 700.00 |

|

|

|

|

Expenses |

|

|

Chemicals |

1 600.00 |

|

Feed |

25 025.00 |

|

Fertilizer |

12 500.00 |

|

Gas, fuel, oil |

15 478.00 |

|

Insurance |

12 587.00 |

|

Hired labour |

4 568.00 |

|

Rent |

12870.00 |

|

Repairs and Maintenance |

2 357.00 |

|

Seeds |

25 478.00 |

|

Supplies |

6 899.00 |

|

Utilities |

264.00 |

|

Veterinary costs |

18 975.00 |

|

Medication |

15 680.00 |

|

Machine hire |

45 000.00 |

|

Interest bank |

2 685.00 |

|

Bank costs |

580.00 |

|

Wages |

60 457.00 |

|

Salaries management |

120 000.00 |

|

Total Expenses |

383 003.00 |

|

Net Farm Income (Before tax) |

– 183 303.00 |

12.9.4.7.2 Record and allocate monthly transactions.

All income and expenses must be recorded on a monthly basis as a cash flow control and income statement. How it is done is not that important, as long as you understand it, and as long as it is summarised in a prescribed income statement format.

There are several open source accounting applications available that you can download from the internet, but you can also design your own Excel spreadsheet to capture and allocate your monthly income and expenses from the bank statements.

What is most important is the correct allocation of transactions from the bank statement, as these items must correlate with the correct enterprise and will assist you at the end of the financial year to compile an exact enterprise analysis on how your enterprises performed financially.

The more detail you put in allocations, the more you can start evaluating and planning for better budgeting in future. For example, you if you receive a bulk payment from the feedlot company for selling, say, 5 weaners to the feedlot, your bank statement will reflect, say, R 21 859.04 under the reference of XXX Feedlot.

Farmer A will be lazy, and only capture the income amount of R 21 859.04 on the income side of his income statement under “sales cattle”.

Farmer Dhlamini is more precise and will also record the amount of R 21 859.04 on his income statement under sales weaners, but on a side-note split down the bulk payment, through using the XXX Feedlot’s voucher to split the income in more detail on the weaner sales card, as explained in module 2 earlier.

On the expense side, an example would be:

The bank statement reflects an expense of R 11 524.89 paid to ABC Cooperative on the monthly running account.

Again, farmer A is lazy and from the bank statement allocated the expense of R 11 524.89 to Expenses ABC Cooperative.

Farmer Dhlamini on the other hand compares the monthly invoice received and paid to ABC Cooperative, and splits the allocation in the income statement in detail as follows:

It must be clear why farmer Dhlamini can now allocate detailed income and costs from the Income Statement to the Cattle Enterprise Budget to evaluate the real financial situation at the end of the financial year, and do much better planning and control than farmer A.

12.9.4.8 Step 6. The Balance Sheet.

The balance Sheet is defined as a “moment snap” of the financial overview of the business, showing the solvency state of the business at the date and time the Balance Sheet was compiled. The balance sheet will change after each financial transaction, for example: the value of market ready cattle will be recorded today under Current Assets, but tomorrow when delivered to the abattoir, the amount due by the abattoir will be displayed under Outstanding Debtors/ Accounts, and when paid next week, the cash will be displayed under the bank balance.

Please refer again to the explanation of the balance sheet as part of compiling the inventory in farm planning, Part 2 of the Beef Farm Production manuals.

A balance sheet provides detailed information about a company’s assets, liabilities and shareholders’ equity.

Assets are things that a company owns that have value. This typically means they can either be sold or used by the company to make products or provide services that can be sold. Assets include physical property, such as plants, trucks, equipment and inventory. It also includes things that can’t be touched but nevertheless exist and have value, such as trademarks and patents. And cash itself is an asset. So are investments a company makes.

Liabilities are amounts of money that a company owes to others. This can include all kinds of obligations, like money borrowed from a bank to launch a new product, rent for use of a building, money owed to suppliers for materials, payroll a company owes to its employees, environmental clean-up costs, or taxes owed to the government. Liabilities also include obligations to provide goods or services to customers in the future.

Shareholders’ equity is sometimes called capital or net worth. It’s the money that would be left if a company sold all of its assets and paid off all of its liabilities. This leftover money belongs to the shareholders, or the owners, of the company.

Assets are generally listed based on how quickly they will be converted into cash. Current assets are things a company expects to convert to cash within one year. A good example is the farm produce. The farmer expects to sell all farm produce for cash within one year.

Noncurrent assets are things a company does not expect to convert to cash within one year or that would take longer than one year to sell. Noncurrent assets include fixed assets.

Fixed assets are those assets used to operate the business but that are not available for sale, such as trucks, office furniture and other property.

Liabilities are generally listed based on their due dates. Liabilities are said to be either current or long-term.

Current liabilities are obligations a company expects to pay off within the year. Long-term liabilities are obligations due more than one year away.

Shareholders’ equity is the amount owners invested in the company’s stock plus or minus the company’s earnings or losses since inception. Sometimes companies distribute earnings, instead of retaining them. These distributions are called dividends.

12.9.4.9 Cash sales

It is unavoidable to sell farm products such as lambs and also sometimes a slaughtered ox for cash. The simple reason is that some customers are cash buyers. The temptation for the farmer is to put this cash in his pocket and to live it up on luxuries.

The danger is that cash is almost never recorded as income on any statements and therefore also does not become declared as taxable income to SARS. All good, but how does it assist you as farm manager if the cash sales (or purchases) are not officially part of your financial records? It does not help you at all, except that you are in a way “bullshitting” yourself…to be frank!

The cost, effort and dangerous risk to transport and deposit cash in the bank must be recognised, but on the other hand also the risk to allow cash buyers on the farm who will know that you have some cash on hand, becomes a dangerous and life-threatening situation.

The moral of the story… do not do cash sales, especially if these are bigger than a couple of thousand rand! Commercial farmers nowadays print business cards with their bank account details on them and encourage such cash buyers to first go via the bank and then come to the farm with a proof of deposit to collect whatever they bought. With cell phones and communication applications such as SMS or WhatsApp, all these arrangements can be made very easily.

If you still have to handle cash, it will be good to keep a cash register of cash received and cash purchases, and then record these transactions on the income Statement as Cash Sales and Purchases.

12.9.4.10 Source documents

A source document is the original record containing the details to substantiate a transaction entered in an accounting system. For example, a company’s source document for the recording of merchandise purchased is the supplier’s invoice supported by the company’s purchase order and receiving ticket.

12.9.4.10.1 The farmers’ own source documents

- Order book

It is a good practice and reference to make a special order with your signature as proof that you have authorised any purchases. This is especially applicable if you buy on a special credit arrangement at the Cooperative, whether it is on your 30-day open account, or on your seasonal production account.

Big Cooperatives also make mistakes and you will have no proof if they document goods or items on your account that you did not order or purchase. Your authorised order document must correlate with the invoice and Goods Received Voucher given to you after making a purchase and these documents must be allocated and captured as soon as possible in the income statement and filed in a chronological order by date.

- Invoice

Everything you sell from the farm must be accompanied by a tax invoice from yourself. The tax invoice must clearly display your own or business name, ID number or business registration number, the address, contact details such as Cellphone number and email address, the date, and very importantly an Invoice number.

The details of the purchaser must include the full names, address, and contact details. The description of the goods or products must be clear, together with the quantity as well as the item price. The total amount of individual items must be calculated and indicated as the amount due.

VAT Vendors:

If your business or you are registered as a VAT vendor, the VAT registration number must also be indicated under the invoice heading, being a TAX INVOICE.

If you are not a registered VAT vendor, you may not use the term TAX INVOICE, but just INVOICE. You must also indicate under the heading invoice in brackets; (This is not a Tax invoice).

- Statements

The Statement is a document that summarises the credit purchases of your clients at the end of the month and will also include interest accumulated due to late payments. Copies of the invoices mentioned on the statement are normally attached as reference to your client.

The Golden Rule!

- Bank Statements

The bank statement is the farm managers most reliable and useful source document. Use it and file it in number and date sequence.

All items and transactions on the bank statement are usually pre-authorised, so accountants normally do not even ask for any other source documents to compile your final statements and tax returns.

All you as farmers must do is to duplicate the bank statement and to allocate the transactions to the correct enterprise budget spending item.

Hints:

- Register your bank account for electronic bank transactions

- Do all payments once a month via internet banking

- Do the first round of cost allocation through clearly naming the own reference as part of the electronic payment, for example, if you pay ABC Cooperative, the Cooperatives reference will be ACC1201Dhlamini. This will enable ABC Cooperative’s accountant to allocate the payment from their bank statement to credit your Cooperative account. Your own reference will be for example “Beef medication”. When you allocate the cost from the bank statement at month end, the reference to “Beef medication’ will assist you to easily allocate the amount to the correct enterprise item, without necessarily going back to the ABC Cooperative Invoice as source document.

12.9.4.10.2 Industry source documents received

When doing normal purchases in the industry, you will receive the following source documents:

Purchases from suppliers:

- Cash invoice: On direct card / cash payment. Capture the goods and file the invoice

- Credit invoice: Control the goods with your own purchase order, capture the goods and file the invoice

- Credit note: A credit note is issued when you successfully return goods to a supplier. A copy credit note will also be added to your monthly statement of account. File with the other documents.

- Statement of Account: A monthly statement of account will accompany all monthly credit invoices and or credit notes. It is a good policy not to pay the bulk amount due on a statement, but to rather pay all the invoices separately. In this way your bank statement becomes a better source document for allocations of cost to the income statement and enterprise budget.

- Good received Voucher: A Goods Received Voucher (GRV) is normally issued to a Wholesale Supplier to a Cooperative, but the Cooperative can also ask you as client to sign a GRV issued in your name.

Livestock sales to an abattoir

- To sell livestock to an abattoir, the farmer first has to register to the abattoir as a supplier with a supplier number.

- The abattoir will issue a standard Declaration of Health Certificate, to be completed and accompany every load of livestock delivered to the abattoir

- Animals transported to the abattoir must be accompanied by a legal Transport permit that must be handed to the abattoir official on request

- After offloading, the abattoir agent will issue a handwritten receipt of type and total of animals offloaded

- After slaughtering, a Slaughter Sheet is issued with the correct information on your name, supplier number, type and total of animals slaughtered, live mass, carcass mass, price per kg and amounts to be paid, VAT calculated, minus slaughtering cost.

- The farmer can consider this Slaughter Sheet as his Invoice to the abattoir, as the abattoir normally arranges and undertakes to pay for the livestock within 14-days directly to the farmers’ bank account.

- Allocation of income must be made to the income Statement

- The Slaughtering Card must be completed and analysed

Livestock sales to a feedlot

- To sell livestock to a feedlot, the farmer first has to register to the feedlot as a supplier with a supplier number.

- The feedlot will issue a standard Declaration of Health Certificate, to be completed and accompany every load of livestock delivered to the feedlot

- Animals transported to the feedlot must be accompanied by a legal Transport permit that must be handed to the feedlot official on request

- After offloading, the feedlot agent will immediately offload all animals over a scale and issue a receipt of type, total and weights of animals offloaded

- The receipt is normally taken to the feedlot administration who will generate a Voucher for animals received, with all details of the supplier, totals and weight of animals, together with the price per Kg live mass, VAT and the total amount due to the farmer. The voucher is signed as confirmation of agreement by the farmer.

- The farmer can consider this voucher again as his Invoice to the feedlot, as the feedlot normally arranges and undertakes to pay for the livestock within 14-days directly to the farmers’ bank account.

- Allocation of income must be made to the income Statement

- The feedlot voucher must be completed and analysed

- Feedlots normally make use of a livestock agent who will do the weighing and purchase agreement with the farmer on the farm, and then arrange for transport and transport permits to the feedlot.